Modeling Credit Risk

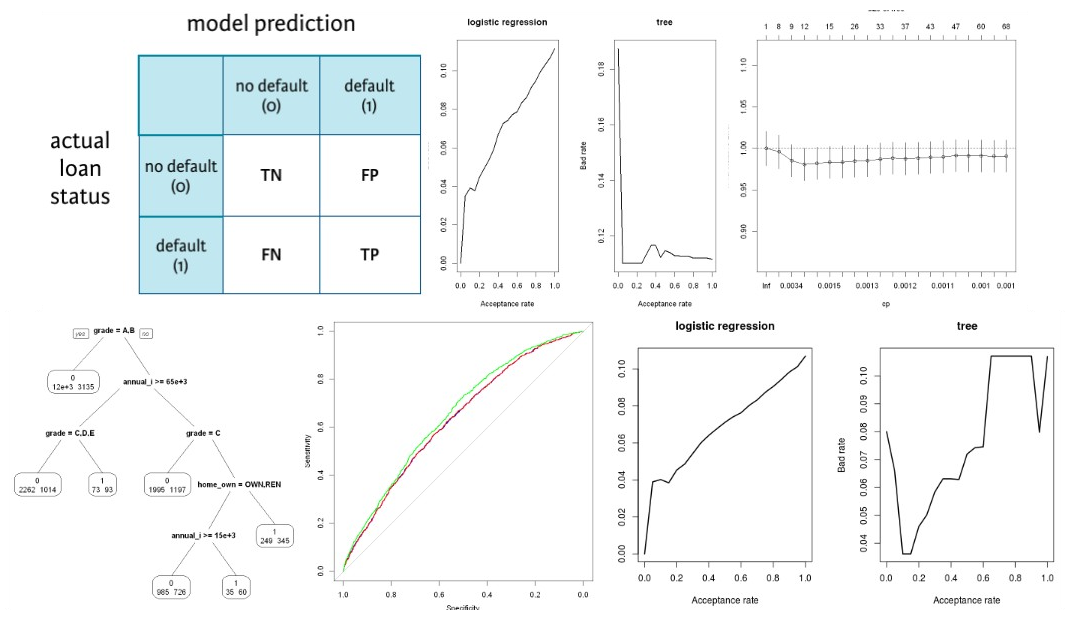

Topics: logit, probit, loglog and decision trees. Descriptive statistics. Train and test sets. Predictions. Confusion Matrix and ROC. Bank loan portfolio acceptance rate, bad rate, and risk tolerance.

Code: R / Tool: Jupyter

Consult the case in a new tab.

This article summarizes a book about predictive modeling and statistical learning applied to credit data. The author repeats the same case study, in 30 variations, using regressions, tree-based, and ensemble methods (as in the case above) as well as Support Vector Machine algorithms and neural networks. Not only can we learn how to implement these techniques, we can compare the procedures and the results as well. Consult the article in a new tab.

The Big Short: a summary of the 2008 financial collapse triggered my mortgage-backed securities (known as the Subprime Crisis). The book was adapted into a comedy movie (a farce).